Securing Mobility

|

| SKT at MWC2019 |

Last year SK telecom announced our True Innovation program (www.true-inno.com) at MWC. True Innovation was founded to make collaborations with SK telecom fast and effective, whether you are a large technology-driven company or an innovative startup. In our first year, we had several successful collaborations in Korea and with global partners.

But more about True Innovation's inaugural year accolades later, having just returned from MWC '19 I wanted to share one of those collaborations in particular: our V2X (Vehicle-to-Everything) Secure Central Gateway. As one of the founding members of True Innovation, I was personally inspired by the overwhelming interest this collaboration received from some of the world's leading auto manufacturers, mobility service operators, and tier-one suppliers. Based on the feedback from several industry insiders, it's fair to claim the V2X Secure Central Gateway is several years ahead of the competition.

The collaboration combines the innovative prowess of two of Korea's high-profile startups Gint and FESCARO, as well as SK telecom's subsidiary ID Quantique. In addition to representing a technological breakthrough for mobility, the collaboration is a symbolic culmination of the past 12 months as both Gint and FESCARO came through SparkLabs, True Innovation's strategic launch partner and Korea's No. 1 Accelerator; while SK telecom also announced the acquisition of IDQ at MWC last year.

The V2X Gateway ensures the safety of passengers by monitoring in-vehicle networks (called CAN buses) in real-time and without omissions for abnormalities. If any unusual activity is detected, this is immediately sent to the cloud where it is analyzed along with information from every other vehicle in the fleet to determine if it is a security threat, and to determine an appropriate course of action. The gateway encrypts both the in-vehicle networks as well as end-to-end communication between the gateway and the cloud, enabling features such as initiating emergency calls, or secure OTA (over-the-air) updates.

How to Lose 30lbs in 3 Months: An Intro to Quantified Self

Disclaimer: I am not a nutritionist, health advisor, doctor or any other type of certified anything in medicine. Any opinions are entirely my own, if you die or get injured after reading this it's your fault.

My Favorite Picture for Summer 2017

|

| My Body Weight: From 205 to 175 in 3 months |

I've spent the past 3 years working as a Project Manager for Global Strategic Initiatives. All the travel, with the lavish lunches, dinners, and early morning breakfast buffets, took a toll on my health. I gained a lot of weight, and although I never entirely stopped exercising my routine suffered.

A few months ago I decided to make some changes. For years I had heard of Quantified Self (QS) and had even dabbled in apps to check my steps, how much I eat, etc. Now it was time to make a concerted effort to test how much of an impact QS can really have.

QS is a broad category that covers all sorts of sensors people can use to track quantitative data about different aspects of their body. There is an essential mantra though, and that is to "support new discoveries about ourselves and our communities that are grounded in accurate observation...." There is a lot going on here... so I decided to just focus on two things: Exercise and Diet. These are the quintessential variables of weight loss, and I wanted to know how much more effective I would be at losing weight by keeping track of them every day.

Getting Started

Since at least the 1950s people have said that weight-loss is about Reducing Caloric Intake while Increasing Caloric Burn. In other words, "eat less, exercise more." Just getting started I didn't want to burden myself with too much information, so I decided to just worry about these two stats.

I had used LoseIt in the past with some success, and I really like the app. So I decided to try using it every day to track how much I eat and burn. It's really easy to do:

1. Download the app and signup

2. Set a weight loss goal: target weight and finish date

3. LoseIt will calculate how many aggregate calories are available to you every day

4. Track everything: food, and exercise

5. BE HONEST: if you go over because of a dinner party, make it count and don't hide it

|

| LoseIt App |

LoseIt includes a massive database of foods including groceries and meal items from international restaurants, has a Barcode Scanner for quickly adding new foods, and will analyse images as well.

Next, I am a huge fan of Strava. While LoseIt has an excellent database of exercises and estimates for calories burned for each, Strava is the best tool for sharing your epic rides, runs, or walks. It's also a good tool to give you confidence in how you are making inputs to the LoseIt app so you can be sure you are tracking the right amount of calories burned.

Being Honest

Be really honest about how much you consume in terms of calories. It will only take a couple nights-out with the boys to realize that alcohol and bar foods are your enemy #1. Likewise, it will only take a couple of breakfast scones and vanilla lattes to realize that sugar-filled pastries and beverages are your enemy #2.

If you are serious about weight-loss, you will quickly overcome these vices. Tracking them will help you acknowledge the problem and deal with it.

Hitting My Stride

The first thing you realise is that exercise will make you hungry, and if you want to combat hunger-pangs you need to find food that is low-calorie and filling. Sweet Potatoes are the champions, but also Light Yogurt, or Soy Milk, and Almonds (not too many) can be great. Sweet Potatoes have a lot of complex carbs so they take a while to digest. Yogurt, Soy Milk, and Almonds have protein and fats that are great for your body.

Fat is fuel, so the goal was to get my body to eat as much of my stored fats as possible. I really didn't know how to do that, but I figured giving my body food that was easy to convert to energy would divert energy away from digestion toward fat-burning.

Bring on the fruits and vegetables that give you lots of energy but are easy to digest.

Putting it in High Gear

After a month I started to see results. I was noticeably thinner and felt better. Feeling better was the most crucial thing. Many of us start to feel pain in our body around our mid-thirties, and this launches us into a vicious cycle of exercising less (because it hurts). However, by eating healthy and exercising daily I started to feel up to more challenges and decided to set some new goals.

These could be anything, but I recommend doing something really awesome like Hiking Across Spain, or Ride a Century.

Since I had started to intensify my workouts with a new goal (I'm going to Spain!), I decided to get the most out of them by going 100% Vegan for at least a few weeks. Living in South Korea, only the most die-hard vegans survive, so I didn't expect to sustain a vegan diet forever. However, this got me cooking ultra lean super foods at home: lentils, broccoli, avocados, etc.

Although I only stayed vegan for a short while, I now prefer seafood and fish, or lean meats in really moderate quantities (around 100 grams). Also, having gone vegan for a few weeks has shown me how amazing that diet will make you feel. I highly recommend making an effort to eat a lot less of meats and dairy products.

Taking it in Stride

After a few months, I have lost almost 30lbs. I'm exercising almost every day, and have added a daily 3x3x30 routine: 3 sets of 30 pushups, squats, and planks. The weight continues to peel-off, though at a more tempered pace. I have allowed myself to reintroduce meat and dairy into my diet, but since I am tracking everything the amount of these foods is greatly reduced.

In short, I look really good, feel even better, eat all the things I love only in more moderate and measured amounts.

Conclusion...

Getting serious about tracking has transformed me. I am a huge believer and have become interested in what other benefits there could be by discovering other areas for improvement. Starting out with the basics, getting a handle over those first is a great idea for anyone. You will see results, promise.

What can I track next? Well, for starters LoseIt has a pro version that allows me to track sleep and water intake. Next, I'm planning to add the new Apple Watch to my repertoire, and maybe Cat Eye computer to track my cadence while cycling.

Is the Mobile Payment Tipping-point Approaching in the US?

If recent surveys regarding mobile wallet use are accurate, the mobile payment boom is about to happen. The next two years could see a rapid adoption of mobile wallets among credit card holders, causing a paradigm shift in the way we make purchases offline and online.

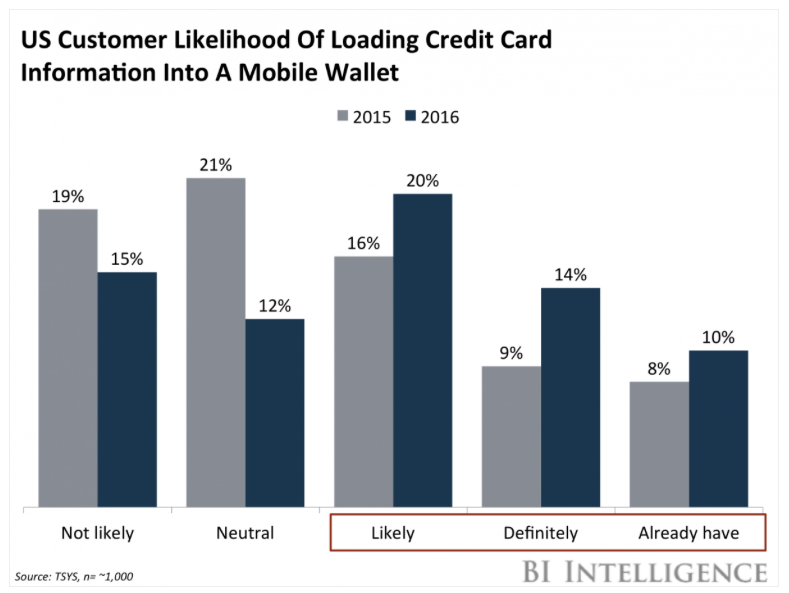

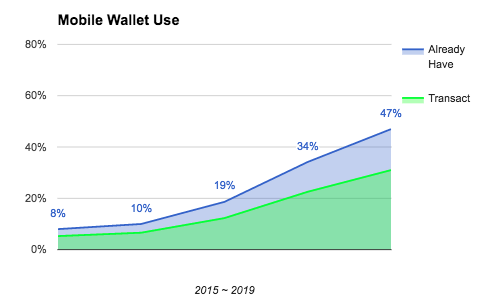

20% of US Customers Are “Likely” to Load Their Credit Card into a Mobile Wallet

According to Business Insider’s Intelligence Unit the potential number of adopters of mobile wallets in the United States, among consumers with credit cards, is growing fast. The survey measured credit card holders’ negative and positive intent to store their credit card information into a mobile wallet as “Not Likely” or “Neutral,” and “Likely” or “Definitely” respectively. They also measured the number of people who “Already Have” stored credit card information into a mobile wallet.

If this data holds true, it’s likely we are on the precipice (FINALLY!) for a mobile payments boom in the United States.

Scenarios for a Mobile Payment Boom

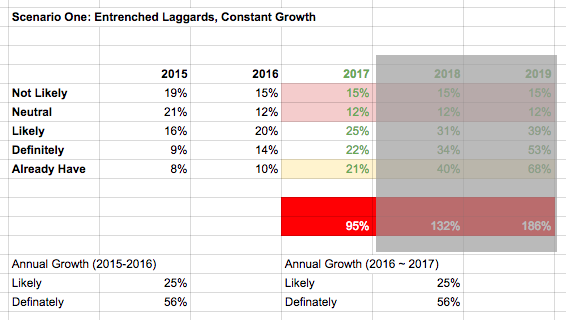

Scenario One: Entrenched Laggards, Constant Growth of Positive Intent

My first impression from this chart by BI Intelligence was that there is a wave of mobile payment adoption coming among credit card holders. However, we need to make some assumptions to see how rapidly this wave is approaching. First, let’s try to get a grasp on the situation.

Key Assumptions:

- 33% of respondents who say they are “definitely” going to load their credit card DO

- 33% of respondents who say they are “likely” to load their credit card DO

- People with negative intent (“Not Likely” or “Neutral”) will remain fixed

- YoY Growth for positive intent will remain constant

In this What-if scenario, we can clearly see that the number of people planning to store credit card information in 2017 will likely increase at a faster rate than previous years. At a constant rate of YoY growth in positive intent only 95% of the population is represented. It is also likely the laggards will continue to decrease over time though we have kept them constant in this scenario.

Furthermore, if we reduce the number of people with positive intent who actually load their credit card -- conversion -- from one in three (33%), the growth rate for people who are “Likely” or “Definitely” going to use a mobile wallet must increase even more dramatically.

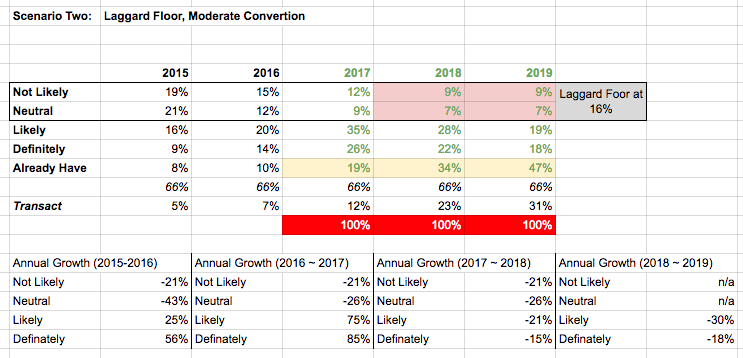

Scenario Two: Laggard Floor, Moderate Conversion

Let’s modify our key assumptions to create a scenario where we have a moderate conversion from intent to action and growth in positive intent, but a similar distribution of responses over time.

However, let’s also assume there is a floor for laggards who show negative intent.

Key Assumptions:

- 33% of respondents who say they are “definitely” going to load their credit card DO

- 20% of respondents who say they are “likely” to load their credit card DO

- The sum of negative intent (“Not Likely” or “Neutral”) cannot be less than 16%

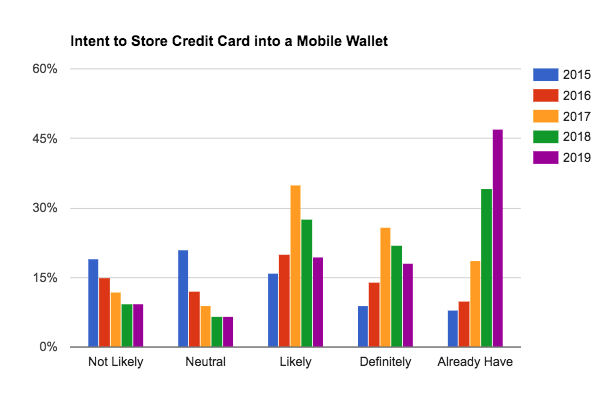

In this scenario we get a picture that’s more believable. We see a spike in positive intent next year, and have adjusted the growth of positive intent moving forward so we get a similar distribution among “Likely” and “Definitely” reponses. At the same time, assuming a moderate conversion rate (one in five, and one in three respondents respectively) among people with positive intent, we see a nice growth curve among those who “Already Have” stored their credit card information into a mobile wallet.

Among those consumers who have already stored their credit card into a mobile wallet, how many do we think have transacted? In general we see a drop in retention of 33% for any major step along an experience. That leaves us at 66% of people who stored a credit card on a mobile wallet, transact with a mobile wallet; which is about what we would expect based on media reports on Apple, Android, and Samsung Pay use among consumers who can use the service.

Does this seem like an aggressive forecast? Not really. If this is correct, it puts consumers transacting with a credit card via a mobile wallet around 30% in 2019.

In other words, half way through the Early Majority stage on the Diffusion of Innovation scale.

Does this mean my Mobile Wallet is about to be really successful?

It’s unclear what success means, but certainly it means a paradigm shift in the way people transact in less than five years. There are many companies banking on this shift, hence the options for consumers are growing as the market is becoming more fragmented.

Currently, most players measure success by number of registered cards, number of transactions, and the value of those transactions. However, profitability for mobile wallets is something still in the future, though certainly that future is less distant today.

How long can you stick in the fight?

Many traditional financial institutions will continue to see their mobile wallet as a value-added service, while customers who are over-served by those institutions will adopt alternatives with superb mobile experiences. Eventually, those alternatives are likely to move up-market taking away more of the retail banking market from traditional financial institutions.

Are you focusing on a superb mobile experience?

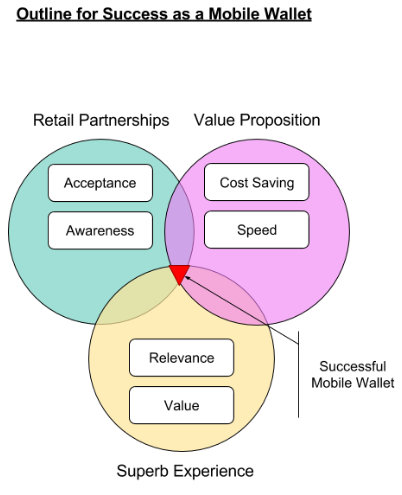

Of course, your payment service is worthless without acceptance. It is essential to have great retail partners who are part of the daily lives of your target audience. And while acceptance is key, so is awareness of your mobile wallet.

Most iPhone 7 users who have a credit card stored on Apple Pay fail to use it because they simply forget it is an option or they don’t know it is. Of course, universal acceptance would resolve this… but until you can get that (please don’t hold your breath) making sure your customers know where your mobile wallet is accepted is critical.

Combining these two critical factors, Acceptance and Awareness, into a superb mobile experience will mean you have a shot at catching onto and riding that wave of mobile wallet adoption.

Can you monetize enough?

The question still remains, how can you monetize your mobile wallet even with a wave of new customers? The recipe for success in consumer-facing mobile payments is still unclear.

There is a plethora of business models and new technologies being experimented with all the time by dozens of players across the payments value chain. Many of these are designed to reduce cost and generate income from that savings, others are designed to create more value by offering discounts or loyalty rewards, while others promise a faster checkout, or try to provide instant settlement.

The list of players is long and diverse. In nearly every country in the world there are several mobile payments players including banks, startups, telcos, retailers, and OEMS. There is a different recipe for each of them.

Ultimately the winners in each market will be those services which can combine Acceptance and Awareness, with a Superb Experience, and a unique Business Model which leverages New Technologies that address cost and speed. I wouldn’t call that a recipe, but perhaps you can call it an outline.

Is RCS Really A Sleeping Giant

Republished from my LinkedIn profile

RCS promises to be a major upgrade to the Native Messenger on your Android smartphone. But is all the talk about a Sleeping Giant over blown?

RCS vs. OTT Messengers

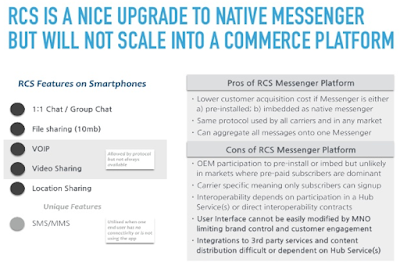

RCS, or Rich Communications Services, is a protocol that's been around for several years. It allows carriers to provide services like Voice and Video Calls, File Sharing (think Photos), and of course Chatting 1:1 or as a Group. The problem with RCS for years was that it requires Interoperability between carriers, otherwise end users can only use the messenger among friends on the same network. These contracts take time and create a complicated user experience (Johnny: "Why didn't you get my text?").

Jibe Mobile created a Hub to allow carriers to create one NNI (Network-to-Network-Interface) with their communications service in order to create interoperability with any other carrier also connected to the Hub, provide they used their white-label messenger (Messenger Plus). They offered colourful skins so carriers could "customise" the user interface. Google acquired Jibe last year, and at MWC a few weeks ago they made some announcements. Yippie!

Google's new platform is great, don't get me wrong. However, it is great as an upgrade to the native messenger available on your Android smartphone if it supports RCS (btw only a fraction of all Android devices currently support it, though that will certainly change). The idea that RCS will emerge as a rival to OTT Messengers like WhatsApp, Facebook Messenger, or WeChat (not to mention Instagram, SnapChat, or anything else new that "tweens" are using) is unfounded in reality, or really optimistic.

The bottom-line is people use OTT Messengers (like other social media) because their friends use it, it's personal, it's unique, and often it's private -- or at least more private than your Google-provided messenger. And more than ever, OTT Messengers are evolving to rival not SMS or other Communication tools, but Operating Systems themselves. They are the new layer upon which all m_commerce is being built... or rather integrated with.

If App distribution was broken before, it's dead now. The tops apps are almost always Facebook, Google, or Apple (or some other usual suspect). Services, both private and public, don't have the time or money to compete with those giants for audience. Enter the OTT Messenger with a dedicated audience that's big and local. On-demand services, eCommerce, traditional businesses, public services, payment (p2p, c2b, and even c2g) can all be integrated to the OTT Messenger. And these integrations can be surfaced, or not, based on wherever the user is. WeChat is a great example of this, and they are pushing into Subsaharan Africa something fierce with their major shareholder Naspers. That's significant in several ways, but in terms of the above examples that means millions of people who are already using their phones to pay for everything. A nudge may be all it takes to put WeChat and Naspers at the centre of m_Commerce there similarly to how WeChat has positioned itself in China.

In addition to services, OTT Messengers are ideal for content distribution which drive downloads for other types of apps. This could be anything, literally.

So sleeping giant? Maybe, those guys at Google are obviously creative and smart. We'll see what they come up with. But on the face of things, Google's new Jibe makes for some fancier Native Messengers, but will hardly impact the impressive rise of OTT Messengers to the centre of our smartphone experience.

Checkout some clips from my slideshare below or see the whole thing:

http://www.slideshare.net/malesniak1/rcs-vs-ott-messengers

http://www.slideshare.net/malesniak1/rcs-vs-ott-messengers

Bluetooth Mesh Networks for Retail

Disclosure: I currently work for SK planet, a wholly-owned subsidiary of SK telecom, one of the companies which sets Bluetooth standards.

The Bluetooth Special Interest Group (SIG) confirmed the introduction of new standards to support mesh networking via bluetooth. There were a few startups like Ubudu and Zuli.io that didn’t wait for the standards and these innovators are the first-movers in creating futuristic customer experiences with bluetooth mesh networks. Now that the standards are out, and it’s a watershed moment for IoT.

Bluetooth Beacon Mesh Networks

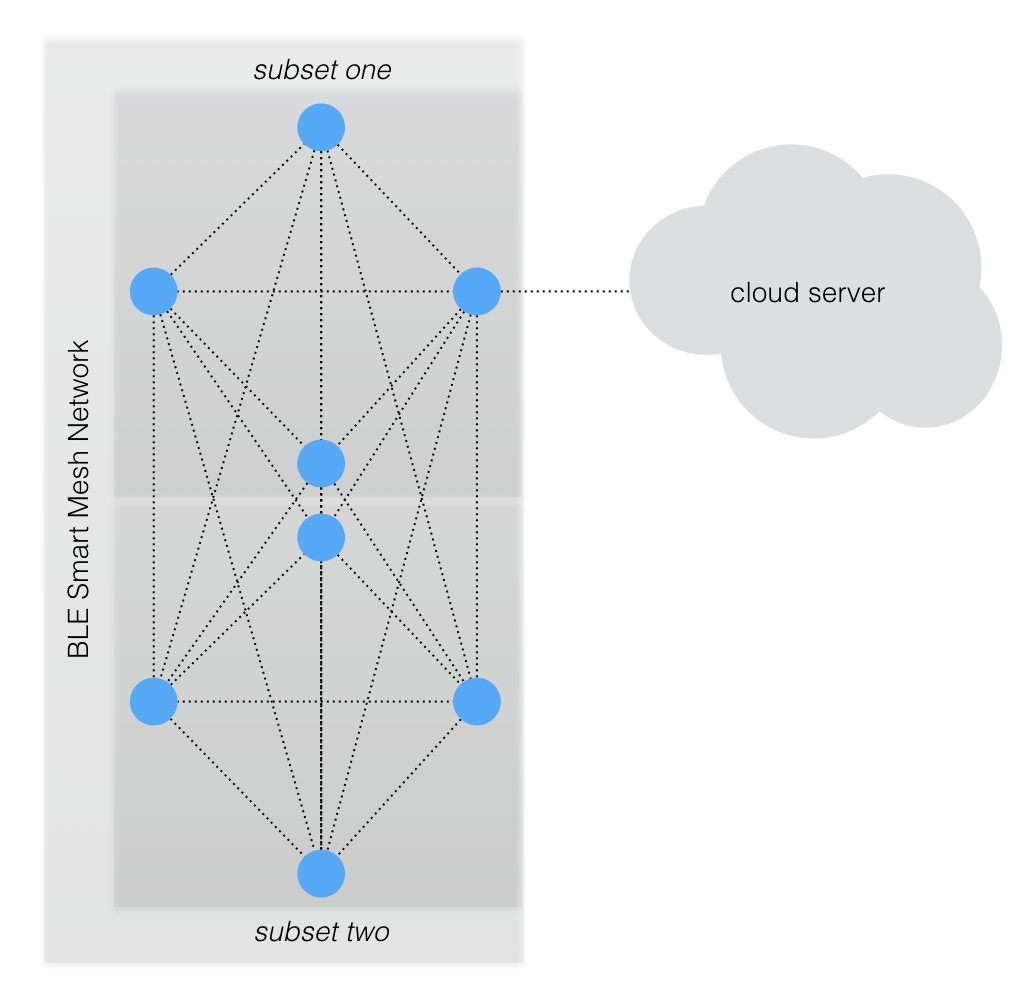

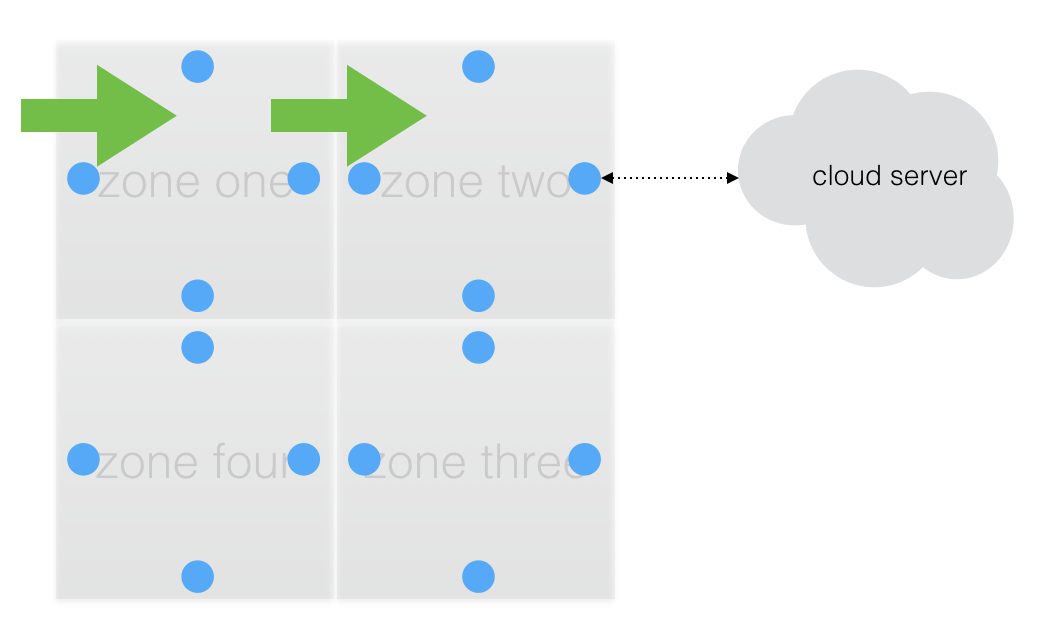

A mesh network could hypothetically extend the range to whatever distance you need. When a beacon is stand-alone it can advertise itself up to a few meters. Even with two-way communication (transmitting or receiving small packets) the potential utility of the beacon is limited to hyper-localised use cases. For example, while near a beacon in a store the client can request specific information about that location from the server; or, perhaps I could use my phone to turn on/off a lamp while near that lamp.

|

| Bluetooth Smart Mesh Network |

A mesh network allows me to extend the range by linking the beacons together. It accomplishes this in two ways: 1) by routing directly to a beacon somewhere in the network to enable a specific experience (e.g. turn-off the kitchen lights downstairs); or, 2) by flooding the entire network or a subset within the network to create an experience using multiple beacons (e.g. set living-room to mom’s profile). Using a mesh network subsets can also be created allowing for unique experiences for connected devices within a specified subset of the network.

Futuristic Consumer Experiences

Smarthomes have been all the rage for a couple years now, and the new standards for mesh networks will accelerate that. However, there are some exciting opportunities for retail consumer experiences as well. Here are a few ideas for implementing bluetooth mesh networks for in-store experiences.

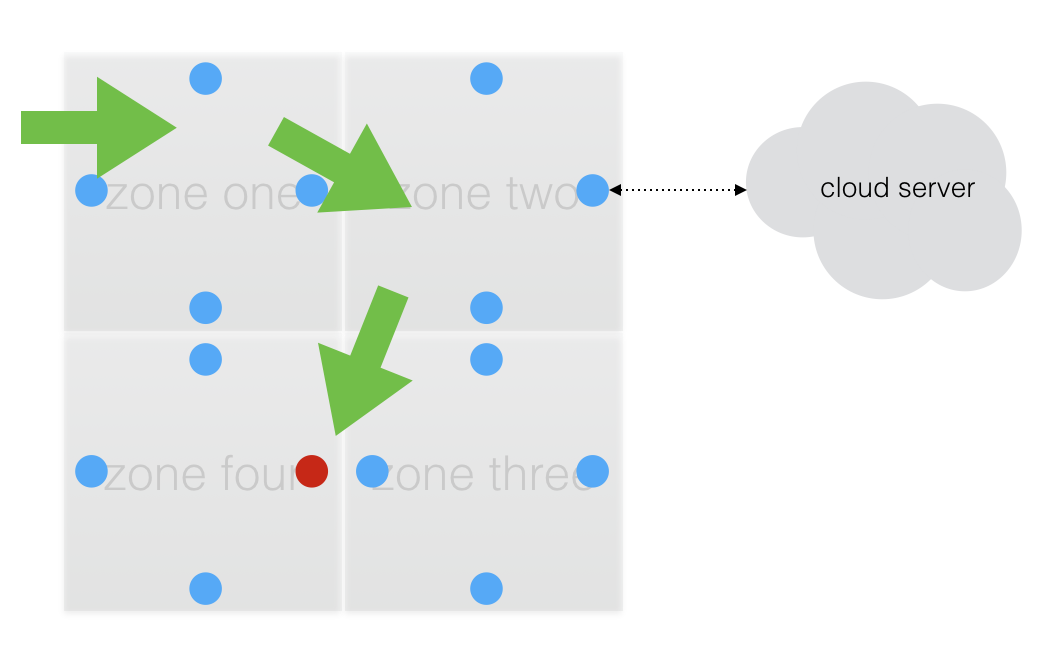

Custom Subsets or “Rooms”

Custom subsets are probably the most well known IoT use case that leverages a mesh network of beacons. This is the oft given example of Smart Homes: dad walks into the living room, the lights dim and TV switches to Bloomberg News. The living room is a subset within the network, and the settings of all devices within that subset can be adjusted to fit the preference of a user. Additionally, a hierarchy of users can be created (i.e. Dad overrides son) and those settings can be engaged simply by walking into a room.

|

| Experiences Adapt To You From Room To Room |

In retail, you can easily imagine this being used to create unique experiences at furniture, luxury audio and video showrooms. The question remains, how is this triggered? An end-user with a smartphone application is the answer most of the time today. Whether or not the use is a customer or salesperson is another question. On the one hand, the lure of customising your own experience while in a showroom could tempt customers to download your software, it may be more efficient to create software for clienteling.

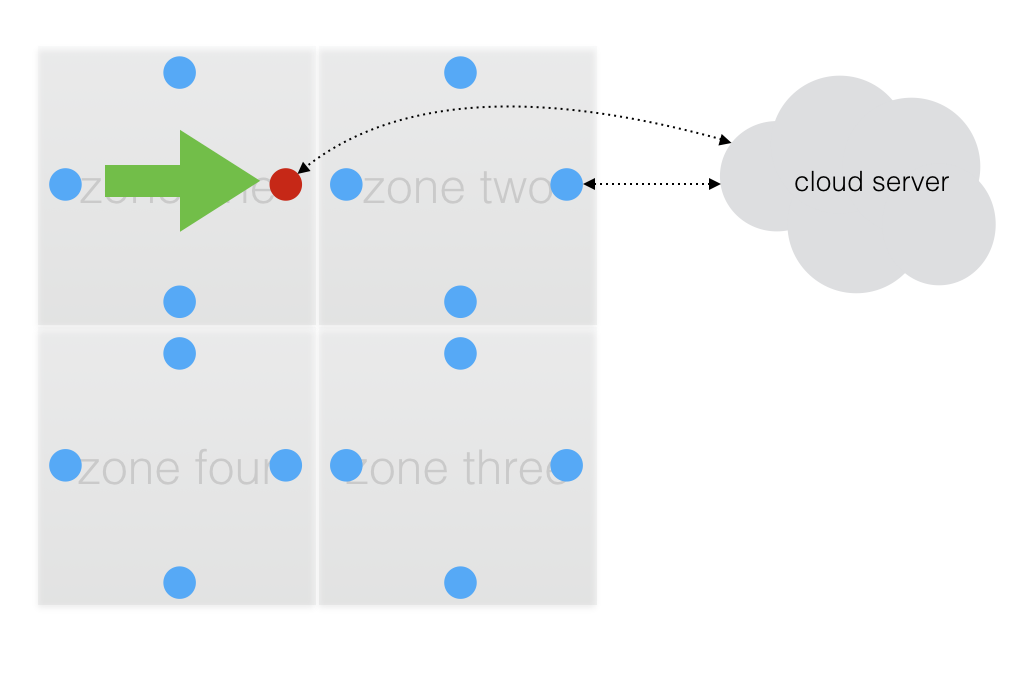

Shopping Efficiency

How much time have customers wasted trying to find products within large department stores, shops within large shopping malls, or the toilet? Networked signage could be used to assist customers and make their journey more efficient. A customer could select the target destination within an app on their smartphone or on a digital sign. As he travels through the store or mall, visual cues can be triggered to guide the customer on his journey.

|

| Signage Alerts When You Arrive |

These cues can be in-app via notifications (“you’re going the wrong way”) or via digital signage (“Customer XYZ here is your destination”). In this use case, a mix of proximity technology like geomagnetics or wi-fi would be the best way to guide customers. However, incorporating visual cues will reassure customers and probably create new opportunities to surprise and delight them.

Personalised Signage & Electronic Labels

Networked Signage and Electronic Labels are another opportunity for retailers and customers. A label which displays a price with e-ink can dynamically display discounted prices to customers subscribed to loyalty programs or with a digital coupon. In fact the packet-size of data needed to display a price is small enough it should be possible without the internet. A networked electronic labels could dynamically generate prices for a section of a shelf, so customer can compare discounts on multiple brands.

|

| Dynamic Prices On Electronic Labels |

More dramatically, personalised media could be presented to customers at any digital sign. Digital Signage connected to a mesh network could request content from the cloud via the network.

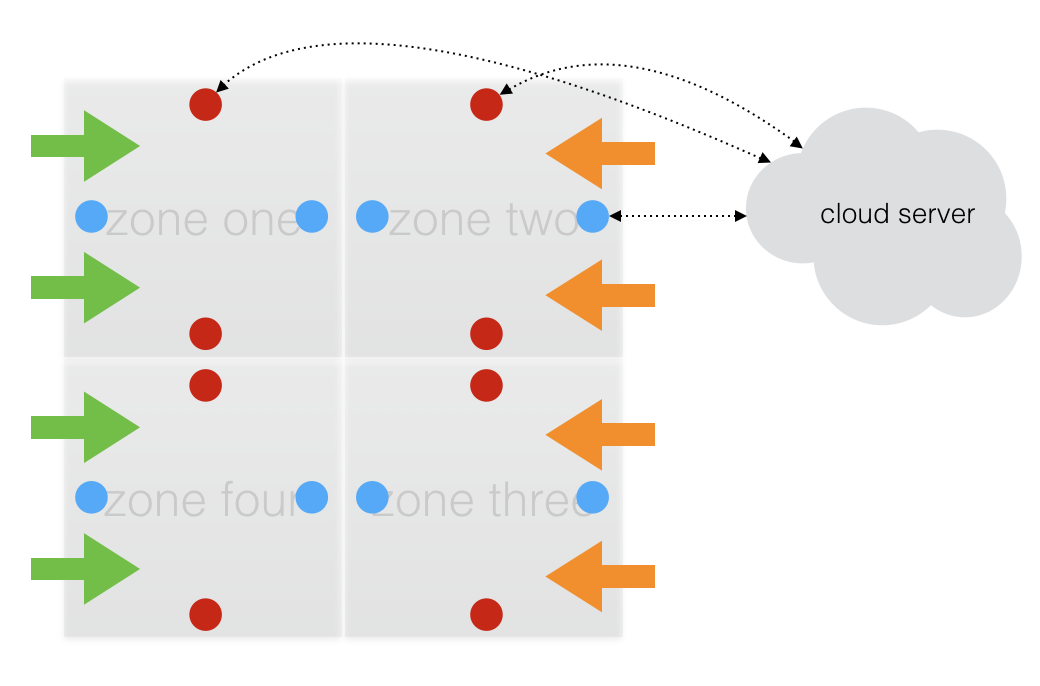

Dynamically Adjust to Audience

With enough connected signage and labels, retailers could abstract further to create experiences for audience types. For example, customers of a given profile at a given time of day within a given store could tend to coalesce within a certain subset of a mesh network. At the same time another group of customers of a given profile could coalesce within another subset. This would allow for digital experiences within either subset to be tailored for those audiences.

|

| Flooding Subsets To Adapt For Audience Profiles (Green vs Orange) |

In Conclusion

Without a doubt the experiences retailers can create leveraging bluetooth mesh networks will be essential to the success of their mobile software. A few technology startups like Ubudu and Zuli, as well as large companies (SK telecom among them) are already moving to make bluetooth mesh beacons a commodity. Digital Signage will be the obvious choice for retail, but the real question will be what unimaginable use cases will creative marketers invent for mesh beacons? I’m not simply referring to engaging content on a screen, but beyond that what new devices will we connect and how will they create more value and efficiency?

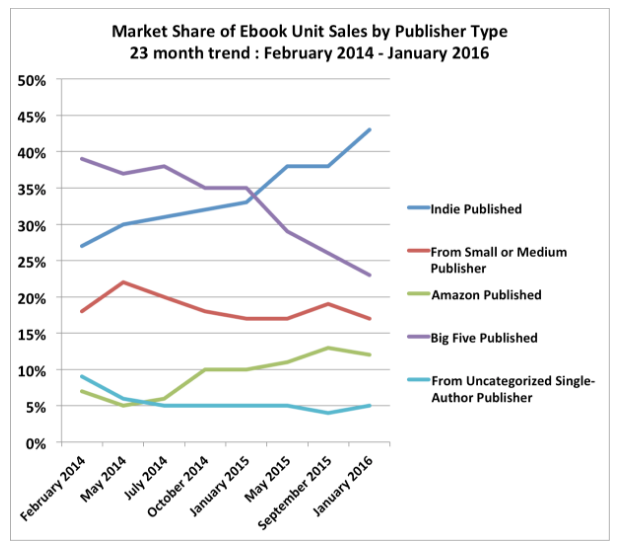

Are Self-Published Authors Earning $1 Billion on Amazon?

Amazon began as an online bookstore. Books were Jeff Bezos answer to the questions “What obvious thing do you know that no one else knows?” He knew there was a longtail of demand for books, that there were people frustrated because either they couldn’t find the books they wanted at their local bookstores or they couldn’t find them quickly. He knew there was a longtail of supply for books, that there was potentially an infinite number of books to fulfill that demand. And he knew people would flock to his webstore if he could provide a solution to connect demand with supply better than anyone else.

While the Everything Store is supposed to have been founded on the premise that the internet would make it easier for consumers to find “Everything” at a lower price, books were the perfect proxy for “Everything.” Books presented a clear problem for both mainstream and niche consumers which could be solved, presented a nearly endless longtail and an eternal shelf-life.

Today the longtail is growing in influence as the power-dynamics of publishing is shifting away from major publishers and into the hands of authors.

The Endless Longtail of Books

The Association of American Publishers (AAP) is “the largest U.S. trade association for the consumer, educational, professional and scholarly publishing industry.” They have for years been tasked with creating standards for publishing, keeping tabs on the book selling industry, and hosting events that bring the industry together to maintain a community of publishers, authors, and distributors. AAP represents publishers, and reports on their performance based on platform (print, or digital) and category monthly and annually. Last year they reported that eBook sales are in decline, and infact they were for publishers.

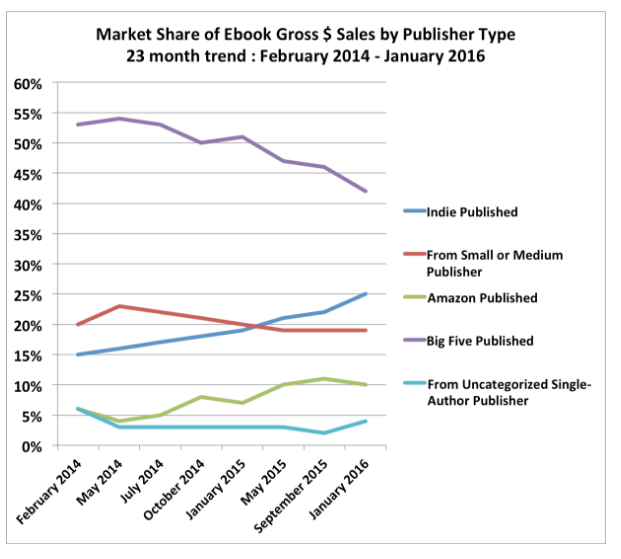

But the real story here was not that publishers represented by AAP are reporting a decline eBook sales; rather, how consumers are choosing to buy independently published eBooks. Fortune, in response to a NY Times article publicizing AAP’s sales statistics as a “plot twist” (that eBooks were in decline while print sales were improving), reported that according to independent industry analysts at Author Earnings the market for eBooks is relatively stagnant though long-term trends favor eBooks becoming dominant over time. What’s remarkable is not the struggle between digital and print, but rather that independent publishers… or self-published authors… now sell more eBooks than the Big 5 publishers who have traditionally dominated book sales.

The ascension of “indie publishers” indicates that a) consumer demand for niche books continues to be strong, b) the quality of indie published books has been or is being syndicated by the masses.

The Writing on the Wall

This shift in dynamics is going to accelerate as consumers earn more trust in authors selling to them directly. Authors already prefer to self-publish in-theory because they can earn substantially more. Selling directly through Amazon means pocketing 70% of the cover price. Selling through a publisher authors typically get 25% of their publisher’s net (for eBook sales). However, cutting out the middleman today still represents an opportunity cost to authors seeking shelf-space offline where 70% of book sales still happen, not to mention abandoning the prestige of making the NY Time Best Seller list.

Arguably many authors today will earn more by sticking to self-published eBooks, but making the NY Times Best Seller list as a self-published author is still unlikely as is getting a deal to produce a major motion picture based on your work. But the dynamics are changing and The Martian is timely example of this, having become both a best seller and a major motion picture.

The Martian was a self-published serial novel that just got traction. Its popularity online caught the attention of Crown Publishing (a division of Penguin Random House) and the rest is history. Success stories like The Martian will certainly inspire more writers to self-publish directly to their audience rather than submit to the complex and onerous demands of the publishing industry.

The Martian was a self-published serial novel that just got traction. Its popularity online caught the attention of Crown Publishing (a division of Penguin Random House) and the rest is history. Success stories like The Martian will certainly inspire more writers to self-publish directly to their audience rather than submit to the complex and onerous demands of the publishing industry.

Better for Consumers and Authors, and Publishers?

Consumers win in this new paradigm of publishing. It means more choice from an increasingly wide range of authors and genres, at a lower cost. Authors win because as they build trust with consumers the more willing those consumers are to pay a few bucks to download their eBook. In fact, authors are set to gain tremendously from this new dynamic. Based on my own back-of-the-envelope estimates self-published authors are approaching $1 billion in revenue on Amazon.

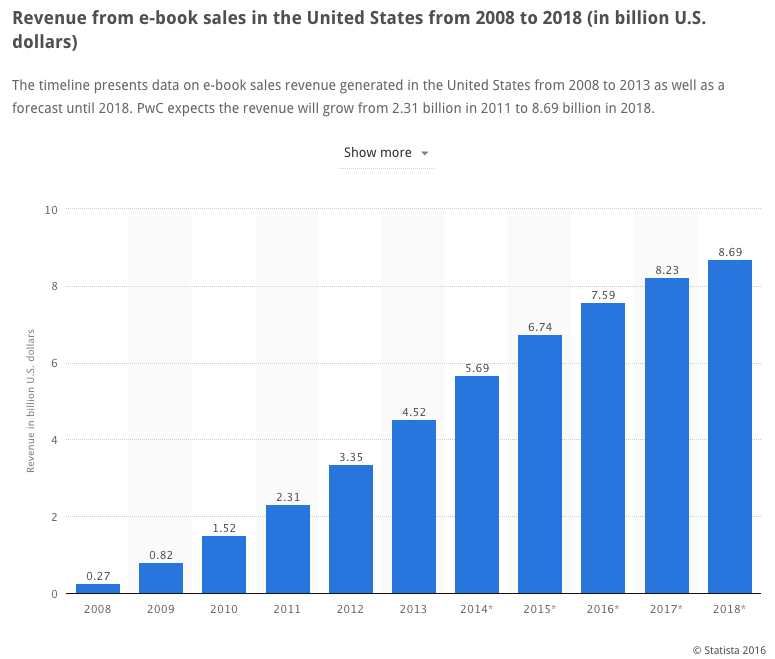

Statista estimates eBook Sales totalled $6.74 Billion in 2015, of which Amazon controls 71% (according to some estimates) giving them $4.79 Billion in eBook Sales. Averaging the percentage of sales per category reported by Author Earnings from January 2015 through January 2016, Indie Published and Uncategorised Single-Author Publishers represent 24% of sales or $1.14 Billion.

Assuming those authors pocket 70% of the cover price, self-published authors earned approximately $800 Million selling on Amazon in 2015.

The question remains whether this will be good for publishers? Clearly it is a better model, allowing consumers to syndicate books first means a more democratic vetting process, less overhead, and higher chances a book will hit the best seller lists once it’s picked up. But that could be temporary, over time the publishers could simply become irrelevant.

RCS vs. OTT Messengers

This is from a post I recently made on LinkedIn...

RCS promises to be a major upgrade to the Native Messenger on your Android smartphone. But is all the talk about a Sleeping Giant over blown?

RCS vs. OTT Messengers

RCS, or Rich Communications Services, is a protocol that's been around for several years. It allows carriers to provide services like Voice and Video Calls, File Sharing (think Photos), and of course Chatting 1:1 or as a Group. The problem with RCS for years was that it requires Interoperability between carriers, otherwise end users can only use the messenger among friends on the same network. These contracts take time and create a complicated user experience (Johnny: "Why didn't you get my text?").

Jibe Mobile created a Hub to allow carriers to create one NNI (Network-to-Network-Interface) with their communications service in order to create interoperability with any other carrier also connected to the Hub, provide they used their white-label messenger (Messenger Plus). They offered colourful skins so carriers could "customise" the user interface. Google acquired Jibe last year, and at MWC a few weeks ago they made some announcements. Yippie!

Google's new platform is great, don't get me wrong. However, it is great as an upgrade to the native messenger available on your Android smartphone if it supports RCS (btw only a fraction of all Android devices currently support it, though that will certainly change). The idea that RCS will emerge as a rival to OTT Messengers like WhatsApp, Facebook Messenger, or WeChat (not to mention Instagram, SnapChat, or anything else new that "tweens" are using) is unfounded in reality, or really optimistic.

The bottom-line is people use OTT Messengers (like other social media) because their friends use it, it's personal, it's unique, and often it's private -- or at least more private than your Google-provided messenger. And more than ever, OTT Messengers are evolving to rival not SMS or other Communication tools, but Operating Systems themselves. They are the new layer upon-which all m_commerce is being built... or rather integrated with.

If App distribution was broken before, it's dead now. The tops apps are almost always Facebook, Google, or Apple (or some other usual suspect). Services, both private and public, don't have the time or money to compete with those giants for audience. Enter the OTT Messenger with a dedicated audience that's big and local. On-demand services, eCommerce, traditional businesses, public services, payment (p2p, c2b, and even c2g) can all be integrated to the OTT Messenger. And these integrations can be surfaced, or not, based on wherever the user is. WeChat is a great example of this, and they are pushing into Subsaharan Africa something fierce with their major shareholder Naspers. That's significant in several ways, but in terms of the above examples that means millions of people who are already using their phones to pay for everything. A nudge may be all it takes to put WeChat and Naspers at the centre of m_Commerce there similarly to how WeChat has positioned itself in China.

In addition to services, OTT Messengers are ideal for content distribution which drive downloads for other types of apps. This could be anything, literally.

So sleeping giant? Maybe, those guys at Google are obviously creative and smart. We'll see what they come up with. But on the face of things, Google's new Jibe makes for some fancier Native Messengers, but will hardly impact the impressive rise of OTT Messengers to the centre of our smartphone experience.

Here is a presentation I put together to compare the two: RCS vs OTT Messengers

Will We Live Forever?

The future is bleak or brilliant depending on who you ask. Whether you consider the displacement of hundreds of millions of people due to rising sea levels, or droughts so severe they force us to abandon entire cities, or food shortages, or the extinction of bees. The list of dystopian outcomes to our collective failure to resolve the most important challenges facing our species is long and intimidating.

Providing a contrary view, futurists like Ray Kurzweil, pioneering entrepreneurs like Peter Diamandis, or visionary researchers like Aubrey De Grey, and ordinary folks like yours truly believe we have a lot to look forward to. Enough to want to live forever, or at least a really long time.

Is this possible? Is it just a dream deferred from a pioneering generation of western yogis and siddhas and vegans? A misplaced optimism instilled in the children of baby boomers throughout western civilization? Can we really live forever?

All Cataclysms Held Constant A Doomsday Lurks

If we hadn’t brought the environment to the brink; if we hadn’t rationalised the deployment of nuclear weapons; if we hadn’t socialised (in the USA that’s subsidize) industries that undermine natural alternatives to chemicals, plastics, coal, oil, etc; if we had been a perfect inhabitant of Earth… we would still be doomed.

Antibiotics have saved lives, tens-of-millions of lives. Penicillin alone is attributed with saving more than 200 million lives. Microbial diseases which plagued families, killing or disabling untold millions of children, have been… well, cured. Today we hardly think of pneumonia or meningitis as life-threatening, and most diseases mean a day-off from work for additional bed rest, tea, and a regimen of antibiotic medicines.

But those days are numbered, the bugs are evolving. As early as 2005 researchers estimated 4% of hospital deaths were caused by antibiotic resistant disease. 25,000 people died a couple of years ago in Europe due to antibiotic resistance strains of disease causing bacteria. More than 10 million people could die each year due to antibiotic resistant disease according to some estimates. Pneumonia, Gonorrhea, Tuberculosis have the potential to be resurgent killers to name a few. In addition to disease, common life-saving procedures become impossible (or life-threatening) when antibiotics fail such as transplant surgery, a burst appendix.

Are we really on the verge of losing our gains in extending life and greatly improving its quality? If we are entering a post-antibiotic era than it seems likely.

Dirt And "Bones"

Doomsday scenarios are both relevant and critical to mobilising people to innovate new ways to cure disease and extend life, and they are successful at doing just that. There is hope, in dirt and "Bones."

First, dirt. More than 10 billion bacteria and fungi live in a single gram of soil. Penicillin comes from one of these, as well as “many other well-known antibiotics.” The challenges has been how to discover new antibiotics from this abundance of microbial life. In fact all the medical achievements of antibiotics have come from just 1% soil bacteria. 99% remains to be explored, and if that is any indication of future discoveries (fingers-crossed) we should be able to combat antibiotic resistance for hundreds of years. Imagine 100 years of drugs without resistance for each 1% of soil we explore… doomsday seems really far away.

A new technology called iChip promises to deliver hundreds if not thousands of new antibiotics, anti-inflammatories, anti-virals, anti-cancer agents, and immunosuppressives. This simple innovation has inspired “citizen scientists” to submit dirt samples from around the United States, soon the world. Combinatory innovation at its finest, a simple new device for sampling dirt combined with unprecedented connectivity to crowdsource new soil samples, thereby exponentially accelerating the process of discovery. Undoubtedly we will have to reform regulatory bodies to facilitate new drugs to become commercialized more efficiently.

So we will overcome resistance, can we live forwever? Well, it is a key part to extending life. There are additional advances in other types of treatments, prevention, and procedures which will help us achieve immortality.

Diagnosis by a medical doctor are only correct 55% of the time, according to the team at Tricorder X Prize, sponsored by Qualcomm. And that’s after you wait 3 weeks to see your doctor, feeling sick and getting worse. Often we are forced to take higher doses of medications to combat diseases that have fester for weeks, and nearly half the time we are being treated for the wrong condition.

Enter “Bones,” Doctor McCoy from Star Trek. Among the new procedures on the verge of emerging from sci-fi lore to real-life are diagnostic tools that promise to make anyone with a smartphone a better diagnostician than a medical doctor. The famed character from Star Trek has inspired inventors to create the solution, a real-life tricorder that can diagnose up to 21 conditions including vital signs, allergens, TB, stroke, and more. The prize has existed for about 3 years, and today there are 10 finalists competing for $10 million. It may be unlikely that any of these companies succeed to diagnosis all 21 conditions this year, but within 5 years it is conceivable our ability to treat disease will radically change.

Will We Live Forever

Undoubtedly there are challenges ahead of us, but the rate of innovation… rather that speed at which sci-fiction is becoming reality… gives us much to be hopeful for. The next gen tricorder could even administer treatments, using programmable nanites. Not to mention regeneration to replace failing organs… but will we live forever?

Maybe, if we can effectively extend life to 95. Some researchers have found that aging effectively stops after 95 years old, and today billions of dollars are being invested to understand how. But living forever at 95 doesn’t sound appealing next to living forever at 25, so researches like Aubrey De Grey are trying to understand if it be stopped sooner. The techno-philanthropists of Silicon Valley including Larry Page, Elon Musk, Peter Thiel, are all invested in efforts like the Palo Alto Longevity Prize and ventures like Calico.

In other words, it is entirely possible that a healthy person today could live significantly longer, and that the first person to live to 1000 years old has already been born. Assuming other calamities don’t end your life, the potential you will live well into your hundreds seems pretty good. Indefinite supplies of effective antibiotics and other treatments, dramatically improved diagnostics, and a host of new tech like nanotechnology, bionics, and regeneration mean that we will at least live long enough to know for certain whether or not we can turn-off aging indefinitely.

Mining Space in 2030

Technologies like nano-bots which can enter your body to repair internal organs or fight disease have captured the imagination of the masses for since the 80s. Remember Inner Space? Mining, is less attractive… it’s downright dirty work. Most of us think of blood diamonds or tragic accidents in West Virginia, and fail to realize just how amazing the future of mining will be. And just how much it will impact our world.

Mining Space in 2030

While the idea of space tourism has been around for years, leisure rides on fancy spacecraft are not what’s driving innovation in space travel: resources are. There are at least two types of resources we know of that are abundant in space. First, the kind that makes deep space exploration possible (i.e. rocket fuel); and second, rare-earth materials.

Making rocket fuel in space is a critical part of deep space exploration, or even mining. The amount of energy it takes to leave Earth is more than the amount it takes to get to moon from Earth orbit. Being able to refuel from space (building in space, say on the moon, would be a next step) would significantly reduce the cost of space travel.

Once we can produce rocket fuel in space then we won’t need to carry the fuel it takes to reach the Moon or Mars (or some mineral rich asteroids) with us on launch. Carrying less fuel, which is really heavy, would dramatically reduce the amount of fuel required to escape Earth’s gravity significantly reducing the cost of every launch. Planetary Resources, arguably the coolest space company out there (sorry SpaceX), has a great video explaining all of this:

Once we can produce rocket fuel in space then we won’t need to carry the fuel it takes to reach the Moon or Mars (or some mineral rich asteroids) with us on launch. Carrying less fuel, which is really heavy, would dramatically reduce the amount of fuel required to escape Earth’s gravity significantly reducing the cost of every launch. Planetary Resources, arguably the coolest space company out there (sorry SpaceX), has a great video explaining all of this:

Critics would argue that science and exploration are not the primary motivations for companies like Planetary Resources (nor their benefactors, among them Google). Rather, they claim they are motivated by profits alone. Perhaps, that's true (though I don't agree). Another abundant resource in space is platinum. Platinum and other rare metals found on Earth come from meteors, and we now have the ability to speculate asteroids to identify which ones are likely to contain them. It’s estimated that just one asteroid of moderate size could contain as much or more platinum than has ever been mined on Earth. Control of these resources could potentially mean a shift power from those who control terrestrial resources to those who control extraterrestrial resources.

That said, while it may be profitable to mine for platinum and other rare metals in space, the motivation for doing is not purely capitalistic. It’s an essential step forward in human civilization, and the technology required to mine space will lead to incredible innovations that benefit everyone.

Lunar Base Stations

The moon could become a critical base for long-term space operations, as well as a source of valuable resources. Turns out that while asteroids are full of platinum and water for rocket fuel, the moon is full of a unique form of helium called HE-3. In fact, this stuff is so valuable it makes sustainable lunar mining operations fueled by robotic space miners hauling in nearby asteroids sound reasonable. That’s because HE-3 is considered a key component of nuclear fusion, and while it is extremely rare on Earth --and extremely expensive at $75,000 per ounce-- it is abundant on the moon.

40 tonnes of HE-3 would power all of the United States for an entire year, without accounting for innovations between now and when it becomes available. The United States, China, and Russia all have plans to build mining operations on the moon. In fact, Russia has announced plans to have a permanent settlement on the moon by 2030 stating “we are going to the moon, forever.”

Current estimates say there is about 1,000,000 tonnes of HE-3 on the moon. There are 35,274 ounces in 1 tonne, and each ounce is worth $75,000… so that is $2,645,550,000 per tonne. So multiply that by a million. The price of HE-3 will come down once we can mine it safely and efficiently, but even even a steep reduction in price-per-ounce would leave lucrative margins.

And that's without considering the iron, gold, and other valuable stuff to be had on the moon. Taking into consideration HE-3, additional resources, and the potential value of more than 600,000 asteroids (and counting) many of which could contain more platinum than has ever been mined on Earth in history, and continuous operations on the moon to mine and refine space resources quickly becomes a priority.

|

Lunar base made by 3-D printers: http://bit.ly/1Dom6hr

|

Moving Forward

Technology is advancing so rapidly it’s difficult to imagine what the world will be like even 15 years from now. That said, what is currently being developed is pretty amazing. Semi-autonomous robots that swarm and work together to complete complex tasks like navigating to an asteroid, confirming it has the desired resources (i.e. water, platinum), bagging and tagging said asteroid, then hauling it back to the Moon where the minerals will be extracted, all the while harvesting the water along the way. That's amazing.

To accomplish this the robots will be at least semi-intelligent, able to improvise and avoid obstacles, and probably learn. Laser communications, Artificial Intelligence, new propulsion systems, advanced solar energy collection and storage, more advanced avionics, data science and predictive algorithms, assembly and materials, not to mention the next duct tape or tang!

To accomplish this the robots will be at least semi-intelligent, able to improvise and avoid obstacles, and probably learn. Laser communications, Artificial Intelligence, new propulsion systems, advanced solar energy collection and storage, more advanced avionics, data science and predictive algorithms, assembly and materials, not to mention the next duct tape or tang!

Naturally, robotic space miners will be limited to the abilities we provide them. The prospect of swarms of space-bots can be troubling though. By 2030 at least four nations could be launching fleets of robotic space miners: Japan, China, Russia, and the United States. While space is abundant, Earth is not. It is within reason to assume that conflicts might arise, but with any luck the abundance of resources in space will be enough to avoid them. Laws are already being written to address the issues around mining and ownership of lunar plots and asteroids.

2015 NRF Big Show Recap

The National Retail Federation’s 104th Annual Big Show was amazing. More than 35,000 executives and the like attended the world’s largest expo for retail. It was my first show, and it was truly awesome. I came back with several new perspectives and insights, as well as reaffirmed confidence in the trajectory of omnichannel retailing. For me, this has been an area of interest for several years so it is exciting to final attend in the Big Show, and see how quickly we are approaching the vision for the Future of Retail -- something many of us have been working for since 2009 or even earlier.

My high level takeaway is that omnichannel retailing is the evolving standard for retail. Retailers will implement a variety of tactics to further implement Omnichannel into their business and marketing operations, with In-Store Experiences central to most aspects of their Omnichannel strategy.

Omnichannel

Omnichannel is an evolving new standard for retail which prioritizes the customer, which requires business practices to adapt to a complex customer journey and marketing practices to adapt to a new “segment of one.”

Fulfillment: Omnichannel fulfillment is a major issue for retailers. This requires Real-Time Inventory accessible from all stores, in-other-words centralized; Distributed Order Management, or the ability to accept and fulfill orders (and update inventory in real-time) from across channels: online, mobile, in-store. This enables drop-shipping from local stores to reduce fulfillment time (online orders); recommendations for local stores where desired inventory is in-stock and can be purchased for pick-up (mobile); have an item shipped from the store, or have an item in a different size, color, etc shipped from a different store for pick-up at a local store or directly to the customer (in-store). Some good examples of omnichannel fulfillment included Netsuite’s “Customer Commerce”

RFID: Omnichannel fulfillment can be implemented without RFID, but achieve the full promise of Intelligent Fulfillment technology such as RFID will be necessary. Real-Time logistics and inventory data, as well as in-store tracking of products and even people (e.g. Intel presented an in-store tracking solution which integrated RFID into a shopping bag), as well as unique customer experiences which simply product discovery and savings.

Segment of One: Aggregating Individual Data combined with Granular Data in Stores, Distribution Centers, and up the Supply Chain will allow for segmentation on an individual basis. This will fulfill the promise of personalization where predictive models based on averages have failed. Technology innovations for real-time inventory and in-store tracking will help, but gaining customers to provide individual data requires stores to innovate around consumer experiences to create value. IBM’s description of Segments of One is comprehensive (if generic), but this goes beyond a profile. Stores and consumer software should provide relevant experiences by determining the context of the store visit: Is she in a rush? Is the dwelling? Is she lost or not sure what to buy?

Actionable Data: Collecting and aggregating data from inventory, in-store tracking, etc., provides information; individual data allows us to determine context which makes data actionable. To gain individual data consumers must perceive value proportional to the risk of providing the information. Value can be created via Savings, Efficiency, and Engagement. Some examples: 78% of customer report they would like to view signs with special promotions (savings), and 67% favor in-store guidance through digital signage (efficiency).

Integrated Data: Breaking down silos is critical to realizing a truly omnichannel store, and the burden rests heavy on software providers. Data must become unified from customer-end to supplier-end and made available to the retailer for real-time analytics. A variety of middleware options to help software vendors integrate data are emerging: e.g. Mad Mobile, Highjump.

Retail Devices

Retailers will purchase a variety of devices that align to their omnicommerce strategy.

Kiosks: A low-hanging fruit for retailers, new kiosks will be installed in 2015 for a variety of use-cases including: bill payment, interactive-tabletop, assisted selling, reporting and personnel management. Both Microsoft and Samsung demonstrated new kiosks, and made partnership announcements: Hardee’s and TGI Fridays will deploy self-order kiosks (Microsoft); Freshwater and ComQi will partner with Samsung to power assisted shopping.

Digital Signage: Arguably the second priority for retailers -- after actionable data -- retailers will quickly adopt digital signage as a low-hanging fruit to implement new in-store experiences as part of their omnichannel strategy. Two of the most impressive exhibits at NRF ‘15 were eBay’s Magic Mirror and Memomi by Memory Mirror (Palo Alto-based startup). Integrating digital signage with real-time data analytics, inventory and fulfillment, and presence technology will be an important part of most retailers omnichannel strategy, if not aspirational since truly integrated and actionable data is still a goal, not a reality, for most (all) retailers. Scala, Lexmark, Toshiba, Samsung, also had noteworthy digital signage exhibits. Lexmark is expected to rollout at Bestbuy, Office Depot, Safeway and 70+ more retailers.

Electronic Shelf Labels: A variant of digital signage, ESL could be a quietly emerging trend. There were two varieties of ESL, one which uses LCD strips to display a variety of content and another which uses e-ink to dynamically display essential information typical to existing labels. The displays can be invoked by presence technology, facilitating dynamic pricing (for example) based on digital coupons stored on a mobile app.

Printer Integration: There were two solutions that addressed our printer integration problem. Ecrebo, a UK based company, which provides an SDK to interface with any printer. The other, Counect, was featured at Intel’s booth and solved the same problem using hardware called Counect Cube. This device operates as a Smart Gateway which utilizes any form of connectivity be-it Ethernet/Wi-Fi/3G/Bluetooth4.0 to interface with the printer and capture transaction data along with customer data.

mPOS: There were a host of mPOS devices from traditional POS players, though Vend and First Data’s Clover were also on site. Retailers will procure devices capable of a variety of payment methods in addition to EMV and Contactless Card. Microsoft Windows 8 POS on notebooks, desktops, tablets and phones were common as well as pairing with iPhone and Macbooks. 1D Laser Scanners, CCD Scanner, 1D/2D Image Scanners, NFC. Zebra Technologies exhibited a variety of Motorola mPOS (acquired), and Korean makers POS BANK and Bluebird had a strong presence.

In-Store Analytics

There is a wealth of information being acquired, and retailers are quickly implementing more strategies to gain better insights across multiple channels and locations. Understanding what is happening in-store is helping retailers improve marketing, assortments (merchandise), staffing, and fulfillment.

WiFi, Beacons, Cameras: Numerous companies exhibited In-Store Analytics solutions which leveraged WiFi, Bluetooth, or Cameras; the majority of them deploying devices integrating one or all of these. People Counting (check-in), Window Display Effectiveness, Customer Journey Tracking, etc. These solutions are packaged as engagement and staff management solutions, but typically were not integrated with inventory, personnel management, or CRM. Some standout companies were Nomi, Airwatch (VMWare), Euclid and RetailNext; however, there is a clear opportunity to provide truly end-to-end solutions. It is also important to note that several data science and analytics companies are forming close partnerships with device (wifi, beacon, camera) manufactures indicated consolidation is possible if not likely.

Retail Growth Strategies

Retailers are eager to grow amidst a global recovery, low cost of transportation of goods (aka cheap oil), and newly emerging markets (Southeast Asia, Africa). With intensified competition from both incumbent online retailers as well as brick-and-mortar retailers they are employing strategies to gain market share and differentiate themselves in ways that go beyond technology.

Diversification: Major retail brands are diversifying their brand with new products and services. For example, Birchbox launched a brick-and-mortar store where customers can take home product samples in addition to purchasing. Ralph Lauren opened a new flagship featuring Ralph’s Cafe, and Lululemon launched men’s line with an in-store grooming parlor.

Going Big: Several retailers presented on strategies for going global. The consistent was to do it, and do it big when you do. Launching 200 new locations as part of a regional expansion strategy was preferred to (for example) 10 new stores in the UK alone.

Storytelling: An extension of in-store experience, retailers will strive to differentiate amongst themselves and -- importantly -- against online retailers by providing a story to customers. The objective is to transform brick-and-mortar into a destination.

Examples of Future Stores

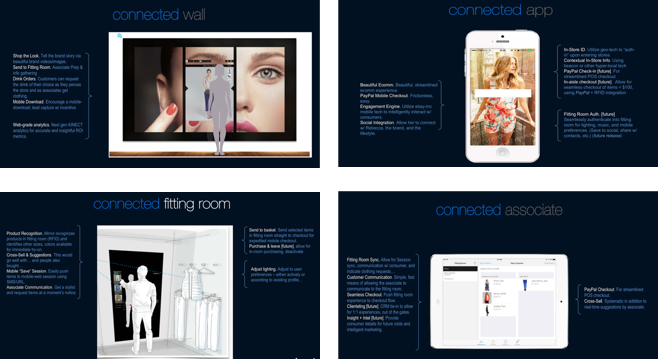

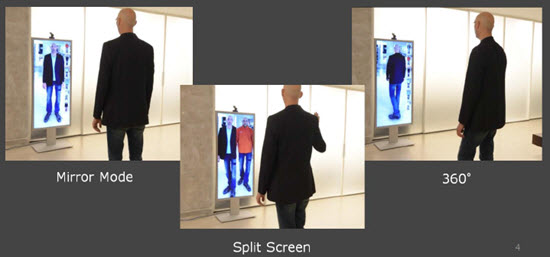

There were a few outstanding examples of technology implementations. Among them, standouts were Rebecca Minkoff, Intel, IBM-Apple, and Microsoft.

Rebecca Minkoff: Hands-down the most complete demonstration of “The Future of Retail” the store implemented useful technology to enhance the In-store shopping experience.

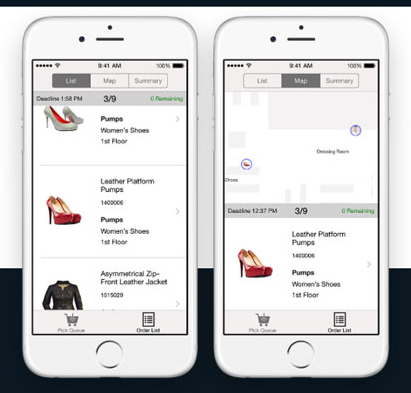

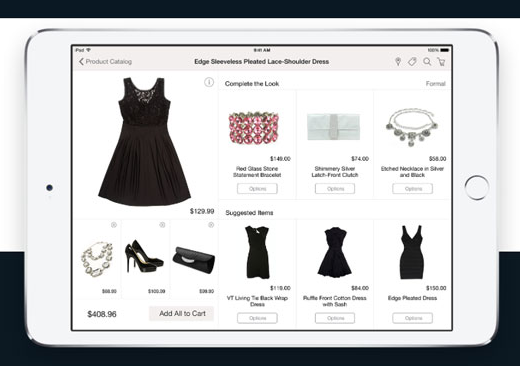

IBM-Apple: IBM launched its MobileFirst for iOS retail enterprise apps Sales Assist and Pick & Pack. Each are powered by Watson, and are part of a new suit of enterprise apps which will include apps for banking, retail, insurance, financial services (insurance), telecom, government, and airlines.

“The Sales Assist app lets sales associates check customer profiles and make shopping suggestions based on purchase histories, as well as check in-store inventory, locate items in-store and arrange to ship out-of-stock items to the customer. The Pick & Pack app, meanwhile, combines in-store proximity-based tech (beacons) with back-end inventory insight to improve order fulfillment, and is 70% ready to go out-of-the-box.” - brandchannel

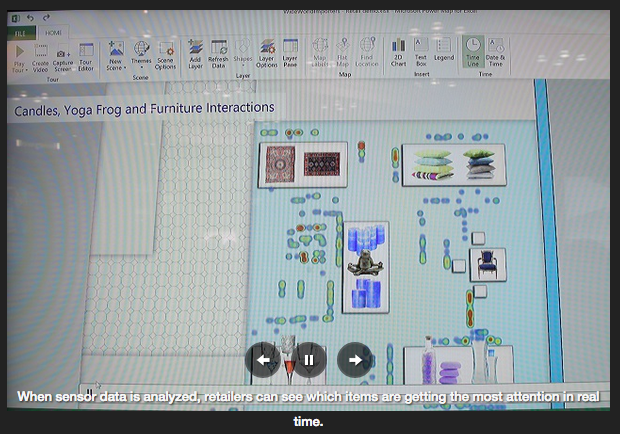

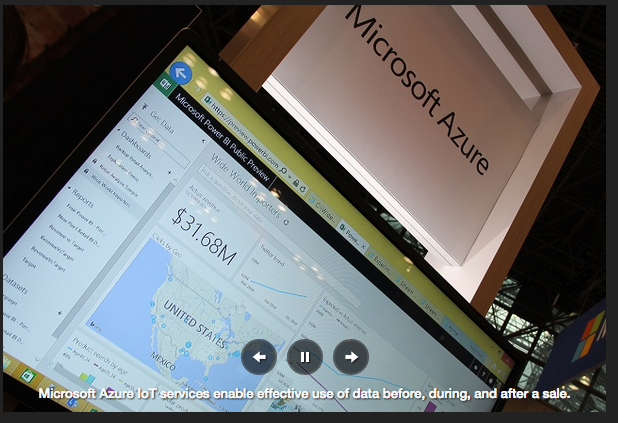

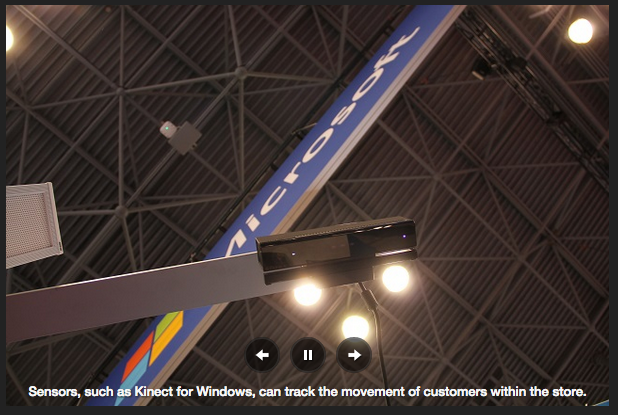

Microsoft End-To-End IoT: Azure HDInsight and Power BI for Office 365 makes it easy for retailers to track revenue, product searches, customer purchasing, social media activity, etc. Can easily access Power Map for Excel to represent responses to online ads, comparing by region or IP. Kinect for Windows is used for in-store tracking of product and customer movement where data is analyzed by Azure Stream Analytics. Azure Machine Learning can make predictions about individual consumers purchasing interests in coming days, weeks, months; and manage inventory in departments, stores, or region. - Microsoft Blog

Conclusion

Though the full vision of an omnichannel store is still aspirational, investments by retailers and vendors are bringing that vision closer to reality than ever before. This new paradigm in retail --a real-time, data driven, customer-focused, destination-creating, renaissance-- is evolving. I guess that means next year I can go back to New York? Hope so!